Who Will Receive the IRS 1099-DA Crypto Form and When Will It Be Issued?

Who will receive a 1099-DA form?

Anyone who has sold or transferred digital assets from a centralized crypto exchange with a tie to the US (e.g., Coinbase, Kraken, Gemini, Uphold, Robinhood, Fidelity, Franklin Templeton, Swan) will receive a 1099-DA.

When will the 1099-DA forms start to be issued?

The first 1099-DA forms will be issued in January/February 2026, covering the 2025 tax year. This timeline is designed to gives exchanges sufficient time to comply (IRS Notice 2014-21).

Note: Decentralized finance (DeFi) users won’t receive 1099-DA forms yet, as DeFi platforms lack U.S. reporting infrastructure. However, regulatory trends (e.g., FinCEN’s crypto rules) suggest future oversight.

Important: Just because you don’t receive a form doesn’t mean you're exempt from reporting. The tax responsibility still exists; the burden simply shifts to you to calculate and report all relevant activity.

What information will be reported on the 1099-DA?

For 2025 (issued 2026): The 1099-DA will report proceeds from sales and transfers, excluding cost basis (what you paid)

However, starting in 2027 (for the 2026): It will include cost basis (if available) and list all trades, transfers, and wallet addresses.

*This means the IRS will see large transaction amounts without knowing if they were profitable.

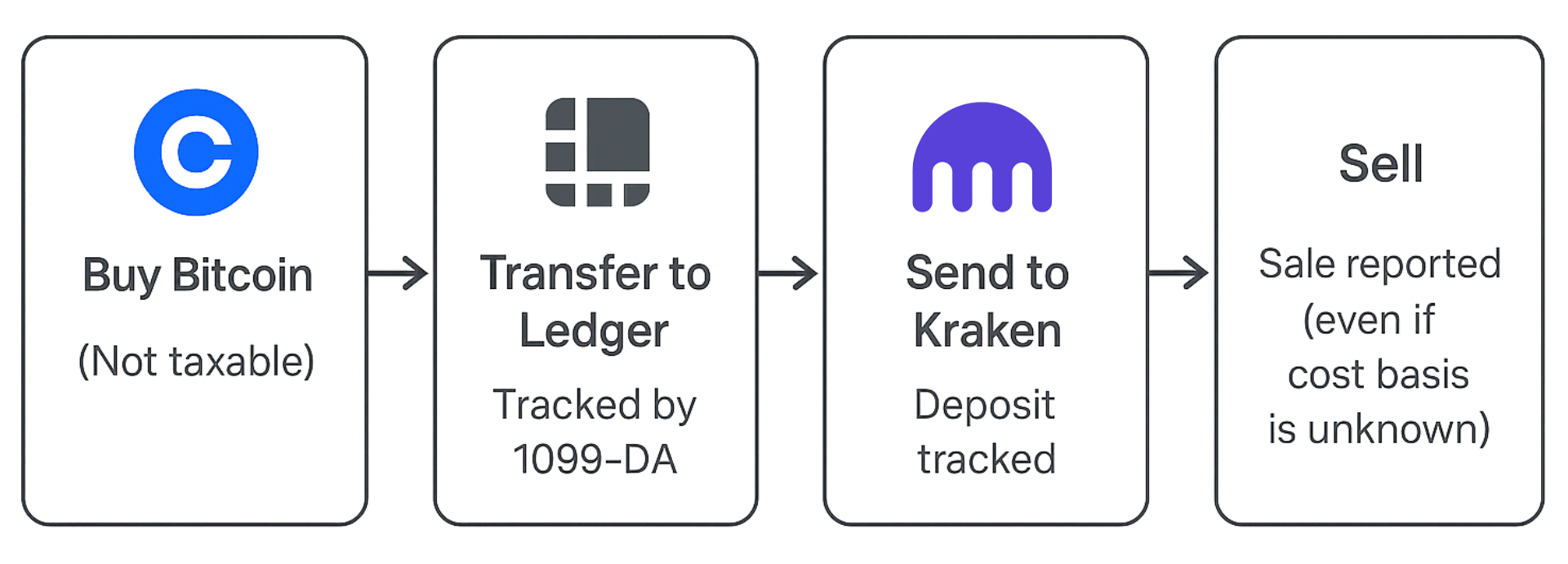

How Wallet Transfers Will Be Tracked

The IRS isn’t just tracking sales, it’s mapping the movement of your crypto through wallet transfers.

Here’s how that works in practice:

Why it matters:

This level of tracking turns what used to be private peer-to-peer transfers into reportable, traceable events. For investors who frequently move assets, the 1099-DA becomes a surveillance tool one that requires precision reporting on your end to avoid misinterpretation.

Note: If you’re participating in our Safe Harbor Allocation Plan, this initiative was designed to align with the IRS’s new 1099‑DA reporting requirements, especially for documenting wallet transfers and cost basis calculations.

What are the risks of not reporting a 1099-DA on your tax return?

Failing to report a 1099-DA may trigger an IRS CP2000 notice, claiming unreported income and issuing a bill. Non-compliance could flag you for crypto tax underreporting, leading to audits or penalties.

How to Prepare for the 1099-DA

Simple Investors:

If you trade on one exchange, cost basis is tracked, similar to stocks.

Complex Investors:

Moving assets across exchanges or wallets complicates reporting.

Records:

Keep detailed transaction records to ensure compliance.

CryptoTaxAudit can help calculate your gains, especially if your situation is complex, and defend those numbers in the event of an IRS audit.

Read More